The government announced a series of steps aimed at providing some relief against the unprecedented commodity price shocks being felt post the geopolitical escalations. Chief amongst these was a Rs. 8 and Rs. 6 cut respectively in excise duties on petrol and diesel prices per litre. Apart from these, a Rs. 200 subsidy on LPG cylinders has been provided under the Ujjwala scheme. Additionally, customs duties are being cut on some inputs for plastic and steel. Finally, export duties are being hiked on items like pellets, iron ore, and some steel products. All told, these constitute a substantial set of measures and come at just the time when monetary policy was turning quite wary of the developing supply side inflation dynamics. Importantly, this also constitutes a signal that government is equally committed to the battle against inflation (media reports suggest more measures may be taken later if required).

Some Observations

A government unwilling to expand fiscal deficit through resisting subsidizing parts of the consumer basket should ordinarily be seen as complementing monetary policy action in curbing inflation. This is because monetary policy acts to curb aggregate demand by weighing down on parts of its components (Private consumption + Investments + Government consumption + Net exports). As can be seen, an expansion in government spending works at cross-currents to this. Thus by extension, a government unwilling to expand deficit is working in tandem with monetary policy. However, a different approach may have been required in case of fuel items and some other essential inputs owing to the risk of cascade of these prices through the entire manufacturing value chain. It is for this reason, presumably, that RBI / MPC members seem to have been encouraging the government to act. If media reports are to be believed, it is disappointment on this front that may have led monetary policy to come on the front foot on rate adjustments. A theoretical question may be asked to clarify the point: Would the inter-meeting hike have occurred if the government had announced these steps ahead of that meeting?

We don’t really know the answer to the above question. Notwithstanding that, with a government now seemingly also focussed on bearing the burden (and after having made a hefty ‘down-payment’ on the same with these latest measures) the pressure on monetary policy should lessen, ceteris paribus. Now this statement needs to be interpreted carefully. After the April policy and before the May inter-meeting hike, the market as per the swap curves was pricing in 275 bps hikes over 2 years from the overnight rate of 3.75% then. Around 75 – 100 bps of these were expected in year 2. Post the inter-meeting hike, however, the market started discounting all these hikes (and a bit more) in year 1 itself. It is possible, though not immediately observable, that the market unwinds part of the frenzied pace of hikes in year 1 that has been priced in post the inter-meeting hike.

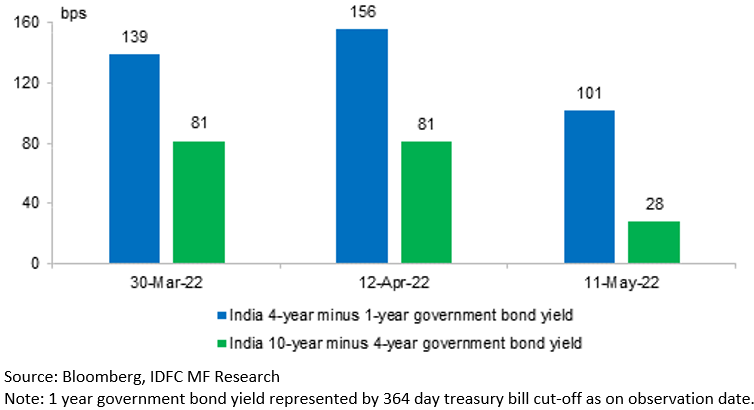

On the bond curve, post the inter-meeting hike there was flattening between 1 and 4 years and between 4 and 10 years. While this makes sense, the residual spread left between 1 and 4 years was still quite large given that the spread between 4 and 10 years had reduced materially. If market was bringing forward all its tightening expectation to the next 1 year, then the maximum flattening pressure should have been felt on the spread between 1 and 4 years. Instead it is 4 to 10 year spread that reduced aggressively while leaving 1 to 4 years reasonably positive sloping. This implied two things: 1> Market was still pricing in higher forward rates ( 2 years and 3 years rates 1 year from now versus where they were currently), thereby still expecting year 2 rate hikes unlike the swap curve. 2> If the reason for this steepness was just bond supply premium on yields, then the 10 year and beyond was heavily ignoring this supply premium. Some of these dynamics are captured in the chart below:

In all likelihood the best explanation for this is simply that most market risk positions were ‘trapped’ in the 4 – 5 year segment and hence this segment felt the most pressure.

Going Forward

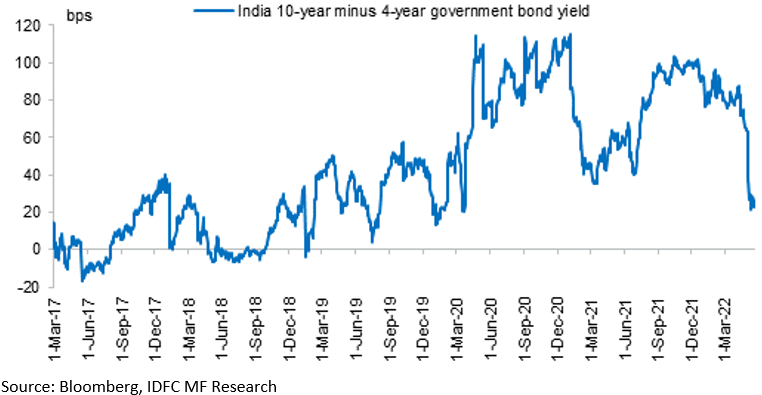

If some of market’s upfronted rate hike expectations were to unwind going forward, then it is logical to expect some giving away also on the 4 – 10 year flattening that has occurred just over the past month. In fact, the market will likely have to price in a larger bond supply premium as well given the new fiscal uncertainties down the line post these (and later may be more) fiscal measures. This will likely put more pressure for this spread to expand. It is to be noted that basis recent action, this spread is now largely in line with the pre-Covid era and is almost completely ignoring the additional bond supply premium that needs to be built in for the new regime of higher government deficit over multiple years. This can be seen in the chart below:

Our long standing overweight 4 – 5 year strategy has been stressed heavily over the past month owing to the market dynamics as discussed above. However, basis our view going forward we think this segment should now start to enjoy a relative tailwind as market partly unwinds rate hike fears and builds back bond supply premium. To be clear, there is little change in our underlying expectation about the likely rate hike trajectory ahead. We continue to think that monetary policy makers want to achieve a position of relative neutrality soon enough. This they seem to have defined around the pre-Covid repo rate of 5.15%. However, unlike the market consensus, we continue to think that the pace of hikes thereafter will be much more measured with the repo rate probably peaking out under the 6% mark. The premise of this expectation, as discussed many times before comes from our assessment of 1> India’s total fiscal and monetary policy response post Covid and the normalisation already underway for monetary policy 2> Our underlying growth trajectory and the characterisation of most of the inflation currently in play 3> Central banks’ having to hike in what is a clearly slowing global cycle and the related point that most of them are unlikely to have a multi-year adjustment runway.

Another observation is noteworthy basis the above. We find a lot of favour in the market today for strategies anchored around the 1 year point. While these may sound ‘surer’ in an otherwise volatile environment, there are nevertheless 2 deficiencies in the argument here in our view:

1> As noted above, 1 to 4 years spread is still very large thus implying quite steep forward curves (3 years 1 year from now, or 2 years 2 years from now if one were to consider 2 years to 4 years spread currently). By focussing on just 1 year (or 2 years) investors are effectively not choosing to ‘own’ these steep forward curves.

2> Investors are potentially courting re-investment risks 1 – 2 years down the line by ignoring 4 – 5 years in favour of 1- 2 years. Even if one were to consider swap pricing (which is excessive in our view) the rate hike cycle will probably be done by year 1. Most likely, given what we think and what we are observing of the global macro cycle, by then the narrative on many central banks would have materially changed. The point about reinvestment risk is especially applicable since, as noted above, the forward curves are so steep. On a related note, tactical products like floating rate bonds may have limited shelf life as well given the nature of this cycle as analysed above.

For investors, we reiterate the view that 4 – 5 year sovereign bonds provide very decent duration-risk-adjusted return for a medium term horizon, and that investors should continue scaling into these over the next few months for those relevant investment horizons.

Disclaimer:

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.

The Disclosures of opinions/in house views/strategy incorporated herein is provided solely to enhance the transparency about the investment strategy / theme of the Scheme and should not be treated as endorsement of the views / opinions or as an investment advice. This document should not be construed as a research report or a recommendation to buy or sell any security. This document has been prepared on the basis of information, which is already available in publicly accessible media or developed through analysis of IDFC Mutual Fund. The information/ views / opinions provided is for informative purpose only and may have ceased to be current by the time it may reach the recipient, which should be taken into account before interpreting this document. The recipient should note and understand that the information provided above may not contain all the material aspects relevant for making an investment decision and the security may or may not continue to form part of the scheme’s portfolio in future. Investors are advised to consult their own investment advisor before making any investment decision in light of their risk appetite, investment goals and horizon. The decision of the Investment Manager may not always be profitable; as such decisions are based on the prevailing market conditions and the understanding of the Investment Manager. Actual market movements may vary from the anticipated trends. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alterations to this statement as may be required from time to time. Neither IDFC Mutual Fund / IDFC AMC Trustee Co. Ltd./ IDFC Asset Management Co. Ltd nor IDFC, its Directors or representatives shall be liable for any damages whether direct or indirect, incidental, punitive special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information.